Santa Monica, CA – Consumer Watchdog called on Blue Shield Thursday to disclose its CEO's salary and justify how it can hold 12 times the surplus required by the state while raising Californians' rates by 59%. Blue Shield is the only major health insurer in California that conceals its top executives' salaries from the public and its customers.

In a letter sent to Blue Shield CEO Bruce Bodaken today, Consumer Watchdog called on the insurer to make key data about the company and its rate hike publicly available. A full copy of the letter is available at http://www.consumerwatchdog.org/resources/bs_letter012011.pdf Unlike most other insurers that are either public companies or traditional nonprofit organizations, Blue Shield's corporate practices are largely hidden from public scrutiny because of its status as a nonprofit mutual benefit corporation. Consumer Watchdog called on Blue Shield to:

* Reveal executive salaries;

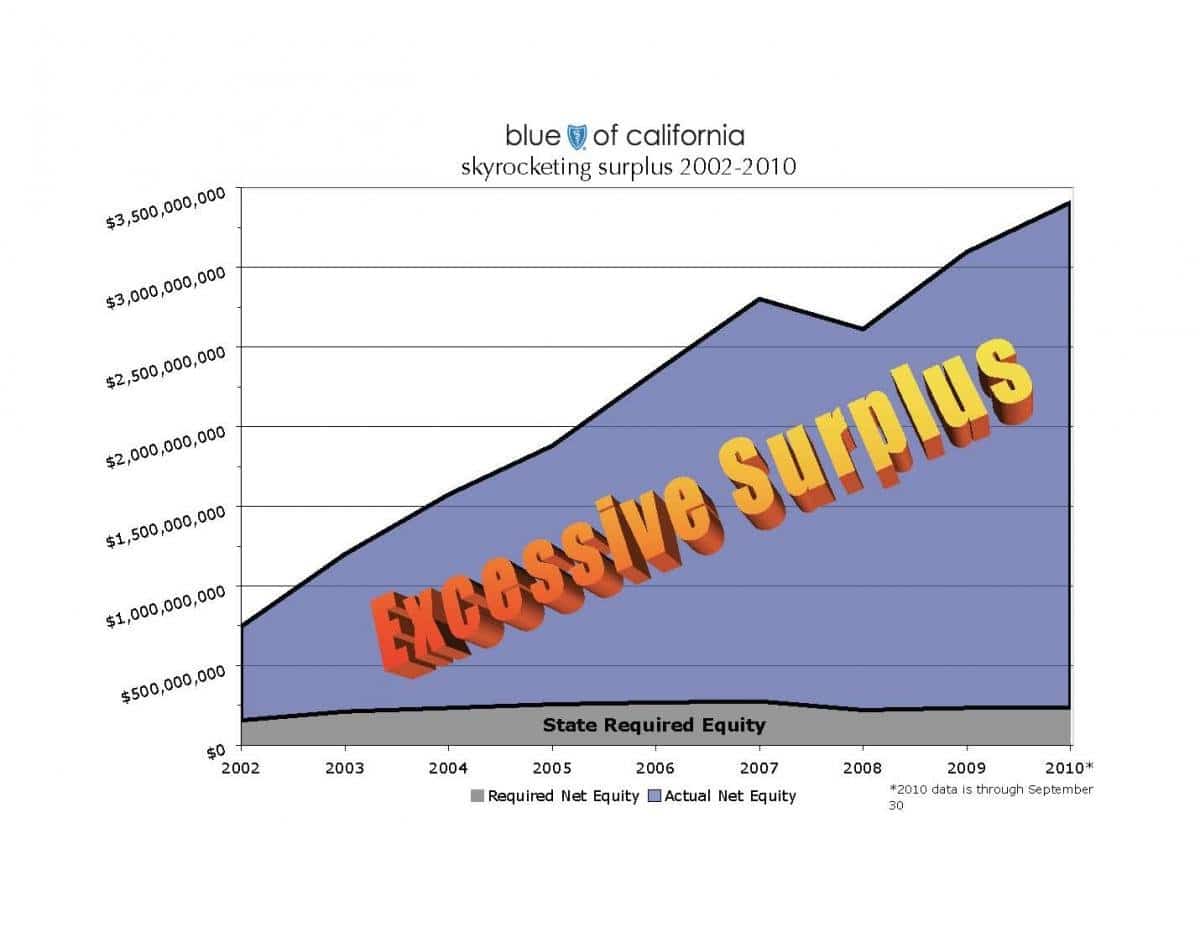

* Justify its decision to grow its surplus to 12 times the amount required by the State of California in recent years; and

* Provide the underlying data and analysis the company claims to have used to support the impending rate hike on nearly 200,000 individual policyholders.

"The burden imposed on hundreds of thousands of Blue Shield customers by the company’s massive rate hikes is almost unfathomable," the nonprofit Consumer Watchdog wrote. "Blue Shield’s refusal to temporarily delay the hikes and submit to a review by the new insurance commissioner also raises serious doubts about the company’s ability to justify increases that will increase some premiums by 59%."

In its letter, Consumer Watchdog noted that the executive salaries of other leading insurers are easily available through public filings, but Blue Shield's are not. It also documented the increase of Blue Shield's surplus, which was about $433 million in excess of the state required "net equity" in 2002. The excess accounts increased nearly sevenfold to $2.93 billion by September 30, 2010, according to the most recent information available. According to filings with the state, Blue Shield's medical expenses did not even double during the same time period. A graph of this increasing surplus is available at http://www.consumerwatchdog.org/sites/default/files/images/bs_excesssurplus.jpg

"Blue Shield has plowed hundreds of millions of policyholder dollars into its equity and surplus accounts rather than returning the excess premium to its customers – members of its 'mutual benefit association' – in the form of lower rates or at the very least stable rates," Consumer Watchdog wrote.

Consumer Watchdog also asked Blue Shield to make key underlying data about the premium hikes publicly available. In particular, the group asked for all the data, along with the corresponding documents and analyses Blue Shield used:

* to project future claims costs and premiums;

* to determine Geographic Area rates and all documents and analyses related to the considerations given to credibility and competitiveness;

* to define the underwriting tiers, as well as the values of the rate multiples by tier;

* to form the basis for the charts “Revenue Drivers 2011” and “Cost of Healthcare Drivers 2011;" and

* to form the basis for Blue Shield's claims trends.

According to Consumer Watchdog, unless the underlying data related to these rates are made available for review, the public cannot know whether the rate hikes have any basis in Blue Shield’s actual experience. The information that Blue Shield has submitted to date regarding its rate hike plan merely provides the state with the company’s own conclusions about its data, without giving the public or officials the ability to determine the validity of the company's assumptions or analysis.

Such underlying information would be automatically made public if Blue Shield faced rate regulation in California, as auto, home and business insurance companies do. Assemblyman Mike Feuer (D-Los Angeles) has introduced AB 52 to require health plans and insurers to receive approval from the state for proposed rate increases.

"As a result of Blue Shield’s rate hike plan, hundreds of thousands of Californians are asking the question, 'How am I going to afford to pay my health insurance premium?' What we ask is 'How did you justify a 59% rate increase?'" Consumer Watchdog concluded in its letter. "Your timely answers to the above questions will allow independent analysts not paid by you to accurately confirm or question your conclusions and the reasoning that led to the increase. It is the least you can do in the wake of setting prices that will leave too many more Californians without health insurance protection."

Consumer Watchdog’s letter to Blue Shield can be downloaded here: http://www.consumerwatchdog.org/resources/bs_letter012011.pdf

– 30 –

Consumer Watchdog — http://ConsumerWatchdog.org — is a nonprofit, nonpartisan organization with offices in California and Washington, D.C.

{kind=link}