The new Republican House majority plowed forward with its anti-health care agenda in DC this week. However, the campaign invective calling for the "repeal" of the job-killing health care bill has officially morphed into “replace” talking points – an explicit acknowledgement that the consumer protections and insurance market reforms in the health reform law are too popular for all but the most reactionary to openly oppose.

I attended a tamer health policy discussion than the one going on in the House, the Health Affairs/Alliance for Health Reform-sponsored National Congress on Health Insurance Reform. Repeatedly, speakers at the three-day event said that a Democratic Senate and Obama in the White House mean that, just like the repeal bill won't get a vote in the Senate, most of the "replace" amendments are unlikely to go anywhere. The exercise is instead a messaging war, intended to prime the public over the next two years for the 2012 elections.

Proponents of reform have to spend that time proving to the public that the bill helps consumers. But what would happen if, rather than just rebutting Republican complaints with more spin, the Democrats put some sweat into actually making the law work? That means not wasting time defending the individual mandate. It's one of, if not the, least-popular provision of the bill, but also the least likely to be repealed because it's the health insurance industry's fondest wish. Instead, Democrats should be taking the fight to the insurance industry.

I was at the conference yesterday to talk about the need for health insurance rate regulation. Premiums are skyrocketing, and getting them under control should be lawmakers' first consumer protection battle of 2011. Certainly, no one looking at a 59% rate hike come March 1 (as Blue Shield of California has announced for some of its 200,000 individual policyholders) is going to buy claims that health reform is protecting them.

The health reform law failed to require rate regulation, and states like California, where the insurance commissioner has no power to modify or deny rates, can’t rein in excessive premiums.

The model for successful regulation of the health insurance industry is California’s “prior approval” insurance regulation law, Proposition 103. It requires auto (and homeowners and business) insurers to publicly justify and get all rate hikes approved before they take effect. It has saved California drivers $62 billion since 1988. Its prior approval standards prohibit excessive rates, funds a consumer intervenor system ensuring a public voice in rate review, and created a publicly accountable elected insurance commissioner.

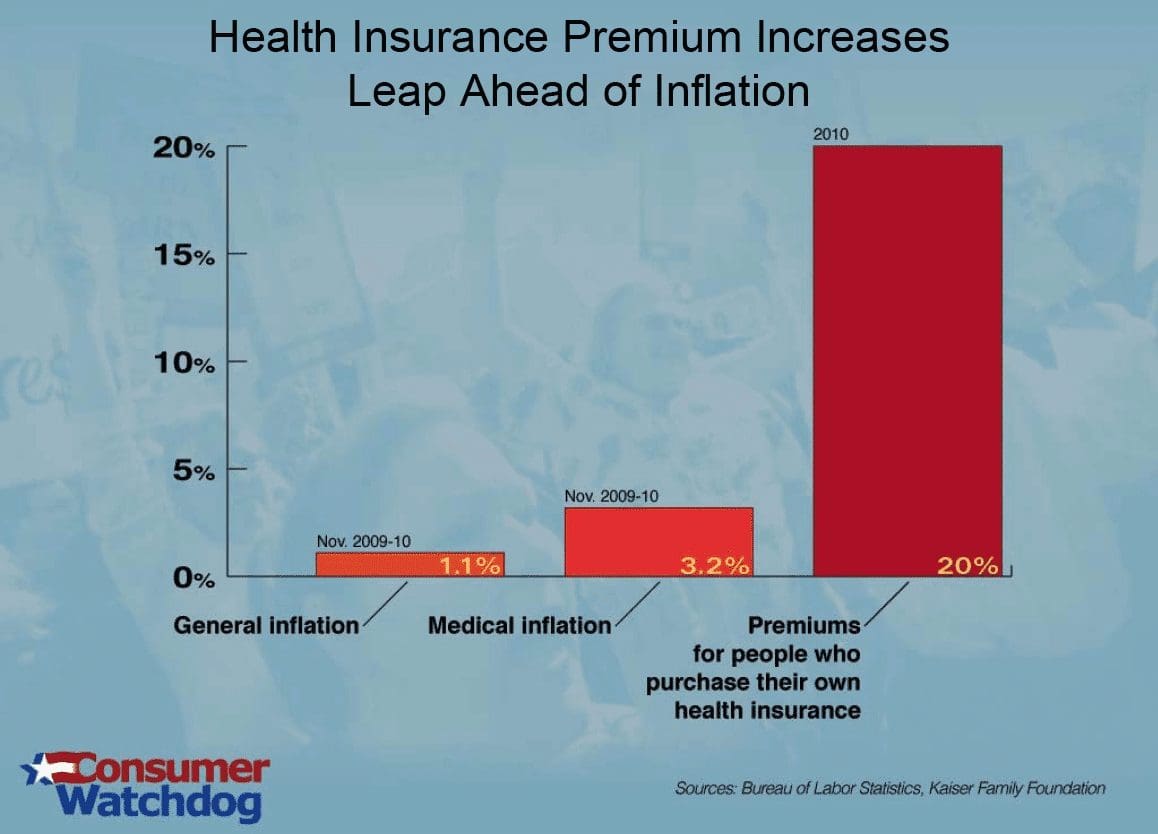

A requirement for regulators to review and reject rates couldn’t come a minute too soon for struggling policyholders. Premium increases are outpacing both wages, and even medical inflation.

The reasons aren't hard to find. Blue Shield of California, for example, is holding 12 times the reserves the state says it needs to be solvent. Download our letter to Blue Shield CEO Bruce Bodaken, demanding he explain why some of that $2.9 billion in extra reserves can’t be used to shield policyholders from the worst of a 59% hike.

States must enact strong prior approval laws that requires insurers to open the books and get every rate approved before it takes effect. Congress should make sure HHS can regulate rates if states fail to act.

All of which was my message to the regulators, policy experts, industry, provider and consumer representatives at the conference yesterday: health reform will fail in the public’s perception, and on the key measure of affordability, without tough regulation of what private health insurers charge.

Download my presentation here: